Open Loop vs Closed Loop Payment Systems: What’s the Difference?

Key Takeaways

Understanding open loop vs closed loop payment systems is the first decision any event organizer or venue operator needs to make before choosing a cashless payment provider.

- Open loop systems use shared networks like Visa and Mastercard — familiar to attendees, easy to deploy, but expensive per transaction and limited in data visibility

- Closed loop systems operate within a controlled ecosystem, giving operators full transaction control, lower fees, and rich behavioral data

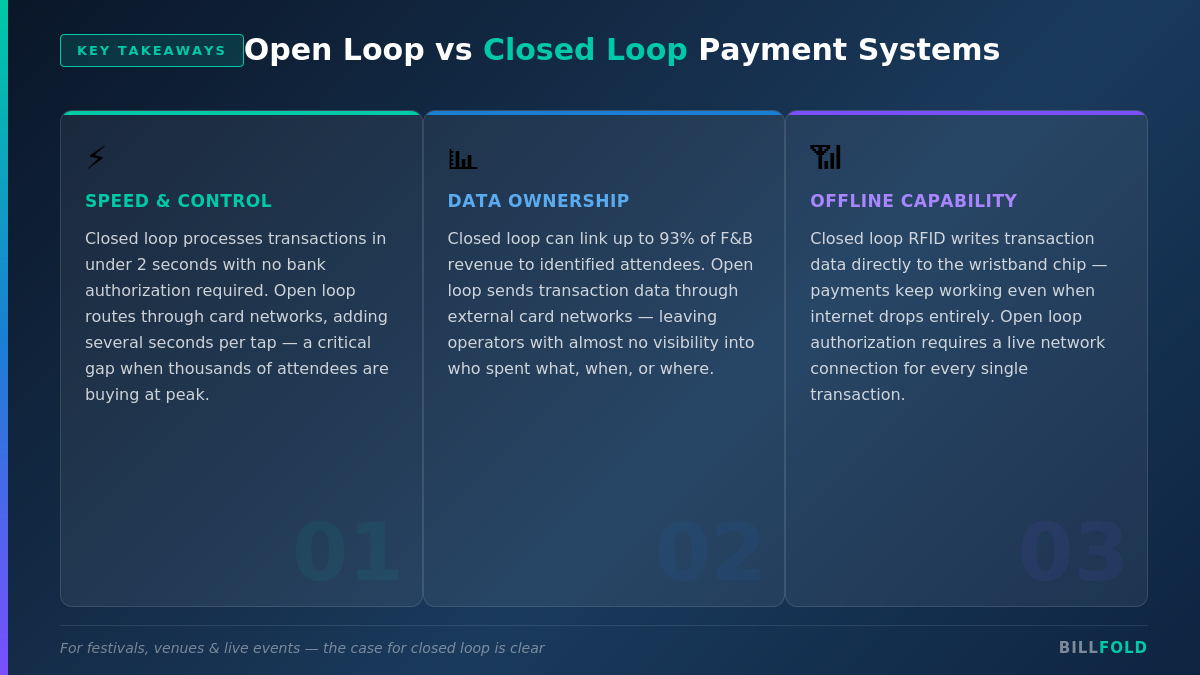

- RFID wristbands are the defining technology of closed loop payments at live events, enabling offline transactions and sub-second speed

- For high-volume events and festivals, the operational and revenue advantages of closed loop models are measurable and significant

If your event runs more than a few hundred transactions per day, the case for closed loop almost always wins on speed, data, and long-term cost.

When you’re planning payment infrastructure for a festival, venue, or large-scale event, the terminology comes fast: contactless, cashless, RFID, NFC, open loop, closed loop. Most of those terms are about the technology. Open loop vs closed loop is about the architecture — the fundamental structure of how payments flow, who controls them, and what happens to the data. Getting this decision right has a direct impact on transaction speed, revenue per attendee, operational overhead, and how much you actually know about what’s happening at your event.

With about half of concerts in the U.S. now cashless, the cashless payment landscape has shifted from novelty to baseline expectation — and event operators who treat this as a generic infrastructure decision tend to leave money on the table. This guide breaks down exactly how both systems work, where each one excels, and why the comparison looks very different for a festival or venue than it does for a retail store.

What Is the Difference Between Open Loop and Closed Loop Payment Systems?

Open loop payment systems are built on shared infrastructure. When an attendee taps a Visa card, uses Apple Pay, or presents a contactless debit card, they’re using an open loop system. The transaction travels through a chain of intermediaries — the acquiring bank, the card network, the issuing bank — before authorization is confirmed. That’s why open loop is sometimes described as the same experience as the high street: it’s familiar, it works everywhere, and it asks nothing new from the customer.

Closed loop payment systems remove that chain entirely. Transactions happen within a controlled environment — a festival grounds, a stadium, a venue — and are processed by a single system operator without routing through external banking networks. Attendees fund a balance in advance (on a wristband, a card, or an app), and every purchase draws from that balance in real time. The operator sees everything. The network intermediaries see nothing.

The fundamental difference isn’t just technical. It’s about who owns the transaction relationship — the card network or the event organizer.

How Do Open Loop and Closed Loop Systems Compare Side by Side?

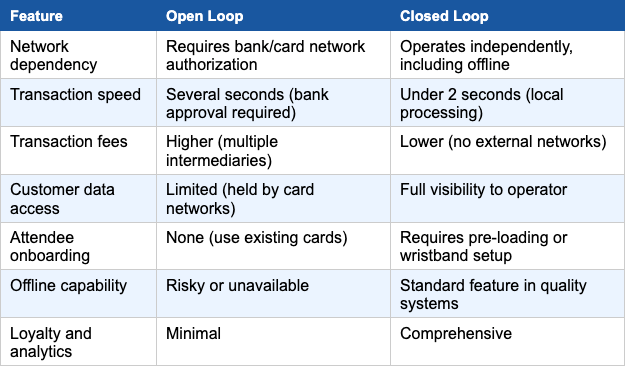

The table below captures the key operational differences that matter most to event and venue operators.

The comparison shows why open loop suits environments where you simply need to accept payment — retail, pop-up stands, simple concessions. Closed loop suits environments where the payment system is part of the operational and commercial infrastructure of the event itself.

What Are the Advantages of Open Loop Payment Systems?

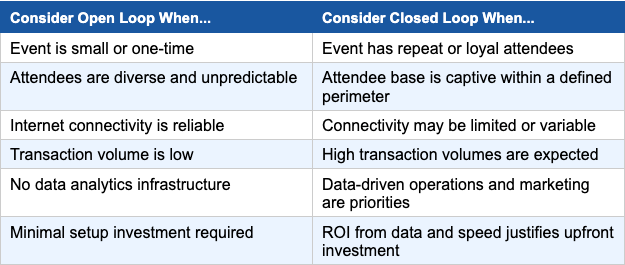

The appeal of open loop is real. There’s no attendee onboarding friction. Someone walks up to a vendor, taps their card, and that’s it. No app to download, no pre-loading funds, no wristband activation. For events with diverse and unpredictable audiences — one-off public events, smaller markets, or pop-up experiences — open loop removes the barrier of asking attendees to change their behavior.

Open loop systems are also simpler to deploy at the operator level. Establishing an account with a payment processor and deploying compatible POS terminals gets you up and running without custom hardware or software. For organizers who don’t expect high transaction volumes or repeat customers, this simplicity has legitimate appeal.

The downside becomes apparent at scale. Every transaction in an open loop system is subject to interchange fees from the card network. At a festival with tens of thousands of transactions, that cost compounds quickly. And because transaction data flows through external networks, operators have minimal visibility into who is buying what, when, and where.

What Are the Advantages of Closed Loop Payment Systems?

For event operators, the advantages of a closed loop payment system tend to stack up in one direction: more control, more revenue, more data. According to Event Industry News, transactions in a closed loop environment save five to ten seconds per payment compared to open loop — a roughly 20% gain in processing time — and across thousands of high-volume transactions, that directly produces shorter queues, smoother service, and higher on-site spend.

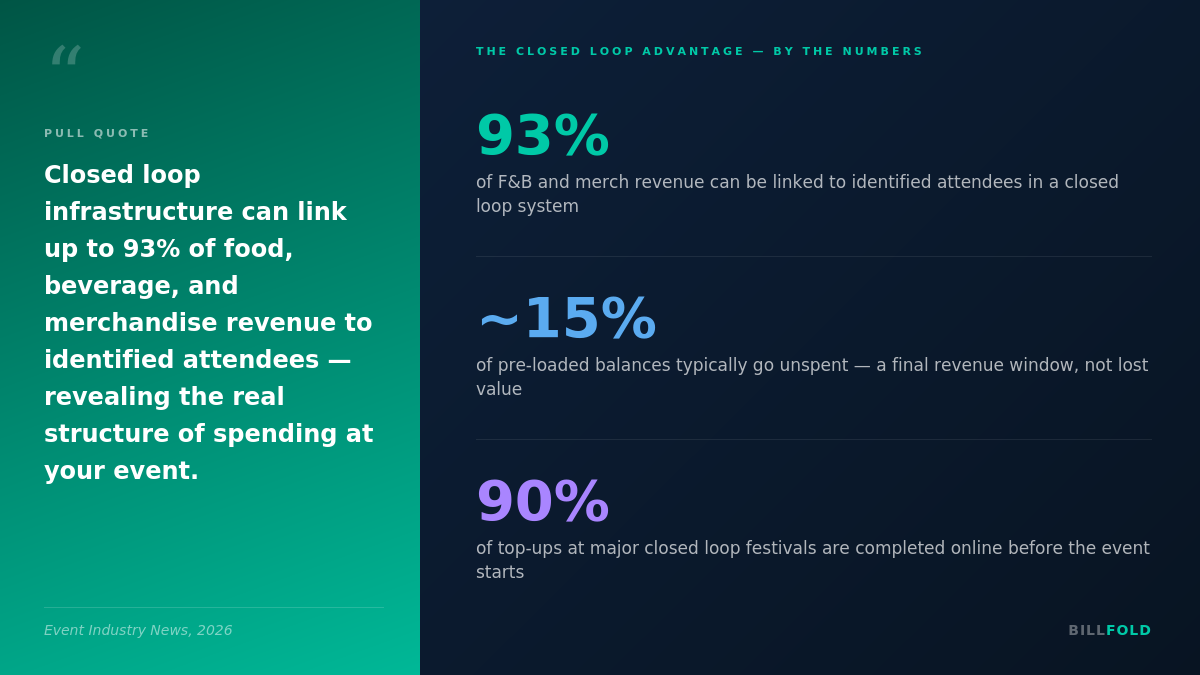

The data advantage is arguably the more durable benefit. Closed loop infrastructure can link up to 93% of food, beverage, and merchandise revenue to identified attendees, revealing the actual structure of spending at an event. That level of visibility is impossible in an open loop environment. It lets organizers identify their highest-value attendees, optimize vendor placement, and build targeted pre-sale campaigns for future events.

There’s also a financial logic that often gets overlooked. Around 15% of pre-loaded balances typically remain unspent at the end of a festival, which creates a final commercial window — a refund deadline or conversion opportunity — rather than being lost revenue. For organizers running tight margins, that unspent balance is genuine additional value that open loop simply doesn’t generate.

Top Reasons Event Operators Choose Closed Loop Payment

- Offline transaction capability — Closed loop systems write transaction data directly to the payment device, so they continue functioning when internet connectivity drops. For festivals in remote locations, this isn’t optional — it’s essential.

- Faster processing — Sub-two-second transactions mean shorter queues and more sales during peak periods.

- Full data ownership — Every purchase is linked to an attendee profile, enabling post-event analytics, behavior mapping, and targeted marketing.

- Lower per-transaction cost — Without card network intermediaries, processing fees are significantly reduced.

- Pre-event revenue — Attendees load funds before arriving, giving organizers cash in hand before a single beer is poured.

- Integrated access control — The same RFID device that handles payments can also manage gate entry, VIP zones, and cashless top-up stations.

- Unspent balance retention — A portion of loaded funds typically goes unspent, creating additional revenue or an incentive to drive early ticket sales for next year.

How Does RFID Factor Into Open Loop vs Closed Loop?

RFID is where the comparison between these two payment models becomes most concrete for festival and event operators. Understanding how RFID behaves differently in each architecture is critical to making the right technology choice.

RFID in Open Loop Systems

Open loop RFID implementations link a wristband or card to an existing bank card or digital wallet. The payment device functions like a contactless card proxy — when an attendee taps to pay, the transaction still routes through the card network for authorization. This means the speed, fee, and data limitations of open loop apply. The wristband looks like event technology but behaves like a Mastercard. For connectivity-dependent venues with reliable infrastructure, this hybrid approach works. But at a large outdoor festival where connectivity is unreliable and queues move fast, the dependency on real-time network authorization creates risk.

RFID in Closed Loop Systems

Closed loop RFID is architecturally different. The RFID chip embedded in the wristband stores an encrypted balance or identifier linked to a pre-funded account managed within the event’s own system. Transactions are written directly to the wristband, meaning they continue to work without a live internet connection. No bank. No card network. No authorization delay. When an attendee taps at a vendor, the system confirms the balance and completes the transaction locally in under two seconds. This is why the world’s largest festivals — from Tomorrowland to Lollapalooza — operate closed loop RFID as their payment standard.

For a deeper look at how RFID technology powers this architecture, the complete RFID payment technology guide covers the technical mechanics in detail, including encryption, tag types, and reader infrastructure.

Which RFID Setup Is Right for Your Event?

The choice between open and closed loop RFID typically comes down to event size and connectivity. Smaller, single-day events in venues with solid infrastructure can operate open loop RFID without major issues. Multi-day festivals, large outdoor events, and high-volume venues should default to closed loop. The RFID cashless payment systems buyer’s guide provides a full framework for evaluating which setup fits your operation.

What Does the Data Say About Closed Loop Adoption at Events?

The event industry’s movement toward closed loop is well-documented. Some of the world’s biggest events — including Boomtown, Tomorrowland, Hellfest, and Lollapalooza — rely on closed loop payments to run complex, high-volume operations reliably. This isn’t a niche preference. It’s a tested operational model.

Around 90% of top-ups at these events are completed online before the event starts, and 80% of festivalgoers top up three times or fewer. The narrative that attendees find closed loop cumbersome or complicated is outdated. Pre-event loading has become a standard part of the ticket purchase flow, and adoption rates reflect that.

The global RFID market data reinforces the trajectory. According to Fortune Business Insights market analysis, the global RFID market is projected to grow from $17.1 billion in 2025 to nearly $37.7 billion by 2032, with event applications representing a significant and growing share of that expansion.

For event operators who want to understand the specific revenue impacts of RFID cashless payment at festivals, the breakdown of benefits of RFID payment for festivals covers per-attendee spending, staffing efficiency, and fraud reduction in detail.

How Should You Decide Between Open Loop and Closed Loop?

The decision isn’t really about which system is better in the abstract. It’s about what your event actually demands.

For most event and festival operators, the decision tips toward closed loop once transaction volume and operational complexity cross a relatively low threshold. The combination of faster transactions, full data ownership, and offline capability makes it the right foundation for running cashless payments at events at any meaningful scale.

Frequently Asked Questions

What’s the simplest way to explain open loop vs closed loop to a vendor or stakeholder?

Open loop means attendees pay with their regular bank card or digital wallet, and the transaction goes through their bank like any other purchase. Closed loop means attendees pre-load funds onto an event-specific device (usually an RFID wristband), and payments happen within the event’s own system without involving external banks. The second model is faster, cheaper per transaction, and gives the organizer full control over the data.

Can a festival use both open loop and closed loop systems at the same time?

Yes, and many do. A common hybrid approach is to accept standard contactless card payments at entry and top-up stations while operating closed loop RFID wristbands for all in-event purchases. This preserves accessibility for attendees who don’t pre-load while maintaining the speed and data advantages of closed loop at vendor points of sale.

Does closed loop mean attendees can’t get a refund if they don’t spend everything?

No. Quality closed loop systems include a refund mechanism for unspent balances, typically processed digitally after the event closes. Operators can also incentivize attendees to spend down their balance before the event ends — which is itself a revenue tactic.

How does offline processing work in a closed loop RFID system?

Closed loop RFID systems write transaction data directly to the wristband chip rather than requiring a live connection to authorize each purchase. This means vendors can continue processing payments during network outages, and the system reconciles all offline transactions when connectivity is restored. It’s one of the key reasons major outdoor festivals favor this model.

Is a cashless loop system harder to set up than taking regular card payments?

The initial deployment requires more planning — hardware provisioning, wristband distribution, attendee onboarding communications, and integration with ticketing and access control. However, once deployed, a well-built cashless loop system typically requires less operational overhead during the event itself, because there’s no cash to handle, no card network failures to troubleshoot, and real-time dashboards replace manual reconciliation.

The Bottom Line: Which System Wins for Events?

The open loop vs closed loop question has a clear answer for most event and festival operators: closed loop wins on every metric that matters at scale. Speed, data, cost efficiency, and offline reliability all favor a well-implemented closed loop system. Open loop has its place for smaller, simpler deployments or as part of a hybrid strategy — but it’s not a long-term foundation for high-volume live events.

The technology has matured well past the early adoption concerns. Modern closed loop systems are reliable, attendee-friendly, and built for the specific demands of festival environments. The question for most organizers isn’t whether to go closed loop. It’s which provider can execute it correctly.

Billfold’s closed loop cashless payment platform is built specifically for live events and venues — combining RFID wristband payments, offline transaction capability, real-time analytics, and integrated access control in a single system. If you’re evaluating your payment infrastructure for an upcoming event, start the conversation with Billfold and see how the numbers stack up for your specific operation.